Most people think wealth begins when you make a lot of money. That is only partly true.

Income matters. A bigger paycheck can make the process easier. But income by itself is not wealth. Plenty of people earn good money and still feel trapped because every dollar is already spoken for before it arrives. The mortgage, car payment, credit cards, subscriptions, food, insurance, taxes, and lifestyle all take their cut.

Wealth begins when you start turning income into something that lasts.

That is the difference between living only from a paycheck and building a financial life with options. The well-off usually understand this difference early. They do not only ask, “How much can I earn?” They ask, “What can this income become?”

That question changes everything.

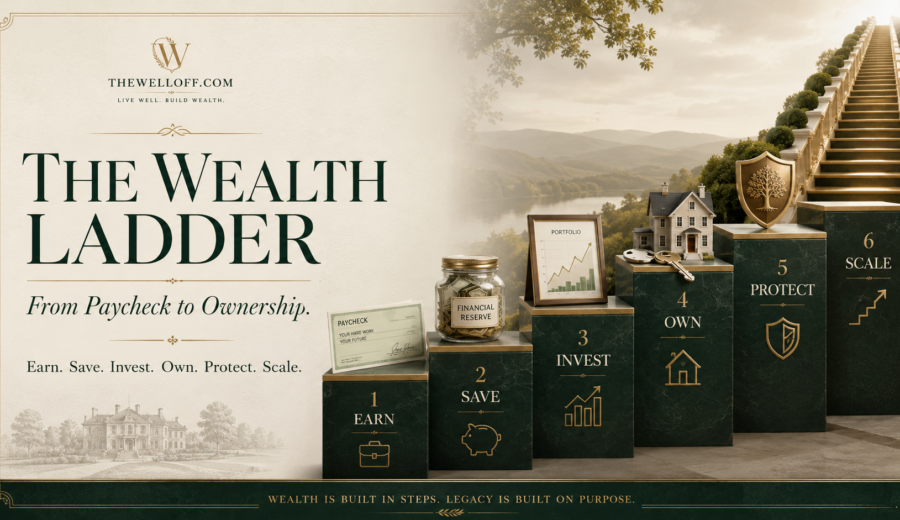

The Wealth Ladder is a simple way to think about the path from working for every dollar to owning assets, building resilience, and creating more freedom over time.

Step One: Earn

The first rung is income. Without income, there is nothing to direct, save, invest, or protect.

For most people, income begins with a job. That is not a weakness. A steady paycheck can be a powerful foundation if it is used well. The problem is when the paycheck becomes the entire plan.

The goal at this stage is not just to work harder. It is to increase the value of your work. That may mean improving your skills, becoming more reliable, learning sales, managing projects, taking on responsibility, changing industries, starting a side business, or building a service people are willing to pay for.

Income is the engine. The stronger the engine, the more choices you have.

But more income only helps if some of it is kept and directed. If every raise becomes a bigger car payment or a more expensive lifestyle, the ladder does not move.

Step Two: Save

Saving is the step where many people begin to feel control for the first time.

A cash cushion gives you breathing room. It helps you handle surprise expenses without turning every problem into debt. It gives you time to think. It lowers panic. It creates options.

Saving does not have to be complicated. Start by separating money before it disappears. Pay yourself first, even if the amount is small. Build the habit before worrying about perfection.

A practical first target is an emergency fund. For some people, that may start with $500 or $1,000. Over time, it may grow into several months of necessary expenses.

The purpose of saving is not to hoard money forever. The purpose is stability. When you have no savings, life can force you into bad decisions. When you have savings, you can respond instead of react.

Step Three: Invest

Saving protects today. Investing builds tomorrow.

Investing is where money begins working beyond your own labor. Instead of every dollar depending on your next hour of work, some dollars are placed into assets that may grow, produce income, or increase in value over time.

For beginners, investing can feel intimidating because the financial world often makes simple ideas sound complex. But the core principle is straightforward: own productive assets, give them time, manage risk, and avoid emotional decisions.

That may include retirement accounts, index funds, ETFs, individual stocks, real estate, businesses, or other assets depending on your situation and knowledge.

The key is not to chase every hot idea. The key is to build a repeatable system. Contribute consistently. Understand what you own. Keep costs reasonable. Avoid risking money you cannot afford to lose. Think in years, not days.

The well-off are not always smarter than everyone else. But they often give their money a job earlier and longer.

Step Four: Own

Ownership is one of the biggest dividing lines in wealth building.

Employees earn income. Owners build equity.

That does not mean everyone needs to quit their job or start a huge company. Ownership can take many forms. You can own shares of businesses through the stock market. You can own rental property. You can own a small service business. You can own digital products, intellectual property, land, equipment, or systems that produce income.

Ownership matters because it gives you a claim on future value.

A paycheck pays you once for work performed. An asset can keep working. A business can grow. A property can build equity. A portfolio can compound. A product can sell more than once.

This is why the Wealth Ladder moves from earning to owning. Income is necessary, but ownership is where long-term financial power begins to appear.

Step Five: Protect

Building wealth without protecting it is like filling a bucket with a hole in the bottom.

Protection includes insurance, emergency savings, reasonable diversification, estate planning, tax awareness, cybersecurity, legal structure where appropriate, and avoiding unnecessary financial risks.

It also means protecting yourself from bad decisions. Speculation, lifestyle inflation, panic selling, overconfidence, scams, and debt misuse can destroy years of progress.

The well-off tend to think defensively as well as offensively. They ask what could go wrong. They build buffers. They avoid putting everything on one bet. They understand that staying in the game matters.

Protection is not fear. Protection is wisdom.

Step Six: Scale

Scaling is the stage where the system becomes bigger than one paycheck.

At this stage, you may have multiple streams of income, growing investments, business ownership, valuable skills, strong savings, and a clearer understanding of how money works.

Scaling can mean many things. It may mean investing more aggressively within your risk tolerance. It may mean hiring help in a business. It may mean buying assets that produce income. It may mean creating products, systems, or partnerships. It may mean reducing dependency on any single employer, customer, platform, or income source.

The point is not to become reckless. The point is to multiply what already works.

Scaling should come after stability, not before it. A person with no savings and high-interest debt usually does not need a complicated strategy. They need a stronger foundation. But once the foundation is there, scaling becomes the natural next step.

Why the Ladder Works

The Wealth Ladder works because each step supports the next.

You earn so you can save.

You save so you can invest.

You invest so you can own.

You own so you can build wealth.

You protect so you can keep going.

You scale so your life is not limited to trading time for money forever.

This is not a get-rich-quick formula. It is the opposite. It is a patient framework for building real wealth over time.

The mistake many people make is trying to jump to the top without building the lower steps. They want investment returns before they have savings. They want business profits before they understand cash flow. They want freedom before they have discipline.

The well-off are not always lucky. Often, they are simply operating from a better map.

Key Takeaways

Wealth is not just high income. It is the process of turning income into assets, ownership, resilience, and freedom.

The Wealth Ladder has six steps: earn, save, invest, own, protect, and scale.

Each step matters. Skipping the foundation can make later success harder to keep.

The goal is not to look rich. The goal is to build a life with more choices, more stability, and more control.

Practical Next Steps

Start by identifying your current rung on the ladder. Are you focused on earning more, building savings, investing consistently, buying assets, protecting what you have, or scaling what already works?

Then choose one action for this month.

That could mean opening a separate savings account, increasing your retirement contribution, reading one investing guide, paying down a high-interest balance, reviewing insurance, starting a side-income experiment, or tracking your net worth.

Small steps matter because wealth is built through repetition.

You do not need to do everything today. You need to start climbing.

Educational Disclaimer

The information in this article is for educational and informational purposes only. It is not personalized financial, investment, tax, legal, or accounting advice. Consider your own circumstances and consult qualified professionals before making major financial decisions.